All the conditions required for further decreases in interest rates are in place: low leveraging, high savings proportion and ample currency reserves. New collective wage agreements create conditions for interest rate decreases, and long-term lower interest rates are one of the greatest improvements in terms for Icelandic households.

In addition, the authorities have issued a declaration regarding the steps that must be taken for the discontinuance of indexation. These will be noted in more detail below.

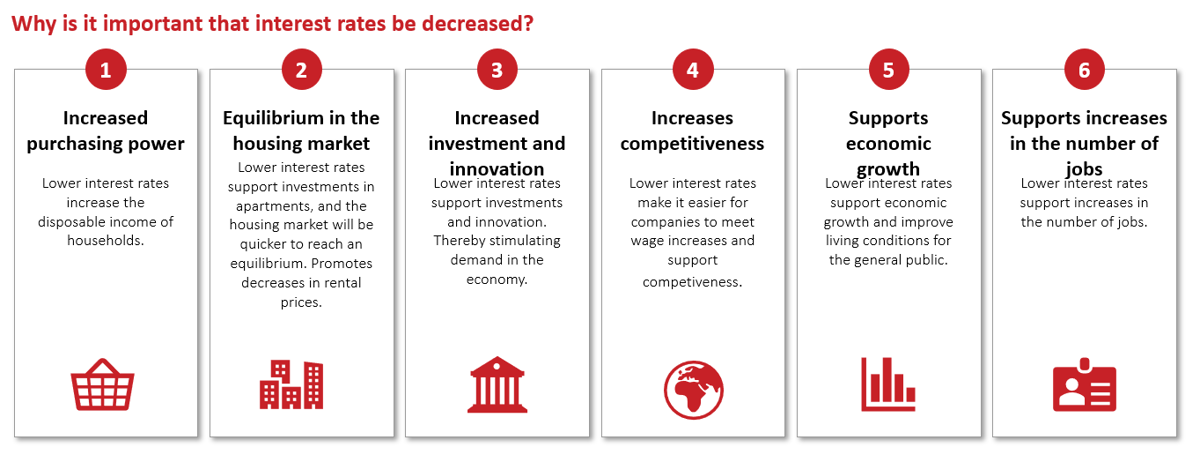

Interest rate decrease

The goal of the living standards agreement is to create conditions for the reduction of interest rates here in Iceland.

Conditions for the reduction in interest rates:

- Sensible living standards agreement effective for four years. Provides for the direct connection between the flexibility of the economic sector to embark on wage changes and wage increases.

- Stable exchange rate of the króna. Unlike earlier downturns, Iceland is now better prepared to tackle economic setbacks. Such preparedness will lessen the likelihood of the devaluation of the Icelandic króna.

- Equilibrium in the housing market. Increased availability of residential housing will continue to reduce rising prices in the housing market.

Indexation

The authorities mention seven issues that are necessary toward abolishing indexation:

- As of the beginning of 2020, granting indexed annuity loans to consumers for terms longer than 25 years will not be permitted except on the fulfilment of certain conditions. The reasoning for this is first and foremost due to the fact that the disadvantage of indexed annuity loans is that price adjustments are added to the principal of the loan and their payment thus deferred. This means that asset formation is slower than it would be otherwise, and the probability that the borrower’s negative equity will increase is greater.

- As of the beginning of 2020, the minimum term of indexed consumer loans will be extended from five years to ten years. This is done to prevent the indexation of all or almost all types of consumer loans, i.e. other than housing loans.

- As of the beginning of 2020, the consumer price index excluding housing will become the basis for indexation in the Act on Interest and Indexation in new consumer loans.

- Before the end of June 2020, the examination of the methodology used in the calculation of the consumer price index based on international comparisons will have been completed and the advice of foreign experts will be sought. The examination will include examining the methodology used when including the housing components as well as the indexation distortion, i.e. the possible overstatement of measurements in the consumer price index as regards systematic measurement inaccuracies.

- Before the end of 2020, a decision must be made on further limitations to providing indexed annuity loans, taking into account premises for stability and interest rate levels. In this context, particular attention must be paid to the impact on the payment burden of low-income households and their prospects of financing housing purchases. This would make it possible to limit annuity loan terms to 20 years or fewer or by establishing a maximum mortgage ratio for indexed annuity loans. Mortgage ratios could change depending on the condition of the economy and may differ according to the arrangement made for instalments, i.e. annuities or equal instalments or according to effective term.

- An examination will be made of increased economic incentives to take out non-indexed loans, e.g. in the form mortgage ratios, tax-free private pension savings and specified assets or that interest rebates apply only to interest and not to price adjustments.

- Means will be sought to curb automatic index increases on goods and services and short-term agreements. Such automatic increases stoke the fire as regards inflation and increase, therefore, indexed debts directly and non-indexed debts indirectly. According to a survey from 2015, approximately half of Icelandic agreements and supplies are indexed. An examination must be made as to whether conditions for price changes must be imposed on contractual relationships which secure the seller’s duty to inform and limit binding periods thereby increasing consumer protection.